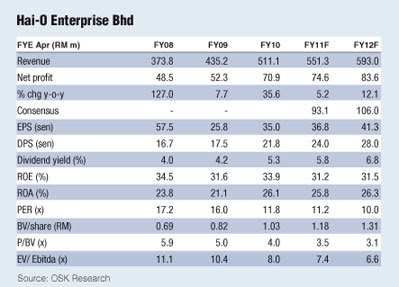

Downgrade to neutral at RM4.12 with reduced target price of RM4.42 (from RM5.03): Hai-O’s FY2010 net profit of RM70.9 million was spot on compared with our FY2010 earnings forecast of RM71.7 million but below consensus’ forecast of RM93.1 million. Full-year revenue rose 17.4% year-on-year (y-o-y) to RM511.1 million while net profit jumped 35.6% y-o-y on better earnings before interest and tax margin or EBIT (+1.3% points y-o-y). Full-year sales at the MLM division surged 19.8% y-o-y while that in the wholesaling and retail divisions inched up by 4% and 6.7% respectively.

Given that the 4QFY2010 topline and profit before tax shrank (PBT) 25.6% and 32.3% y-o-y respectively, the impressive full-year y-o-y revenue and profit growth were mainly attributed to the strong 9MFY2010 results.

The better showing was also driven by higher rental income from leasing in Klang and a lower effect tax of 24.8% versus 30.1% in FY2009.

While 4Q’s results are usually strong, this time around, 4QFY2010’s y-o-y revenue and PBT fell 25.6% and 32.3% respectively, dragged down by the MLM division, which reported a 35.5% y-o-y contraction in sales, although this was partially offset by strong retail sales growth of 44.7% y-o-y.

The MLM division was impacted by slower membership growth which in turn was affected by: (i) the more stringent rules on new member recruitment set by the authorities, and (ii) reduced appetite for loans following the rise in interest rates recently.

On the other hand, the retail division recorded historical highs in sales and profit, mainly attributed to the (i) success in promoting in-house brands — y-o-y EBIT margin improved 6.9% points in 4QFY2010; (ii) the Chinese New Year festival which fell late this year and coincided with the year-end members’ sales promotion. On a quarter-on-quarter basis, revenue and net profit declined by 24.7% and 20.8% y-o-y respectively, due to the poor performance from its MLM division.

We cut our FY2011 and FY2012 earnings forecast by 12% to 18% to RM74.6 million and RM83.6 million respectively, to factor in the slower growth from its MLM division.

Hai-O has proposed a final dividend of 10 sen and a single-tier dividend of 4.5 sen, bringing the total full-year gross dividend to 21.8 sen. — OSK Investment Research Sdn Bhd